1,477 words. Six-minute read.

Since September 2008, Fannie Mae and Freddie Mac (the GSEs) have been wards of the government, placed into conservatorship under the authority of the Federal Housing Finance Agency (FHFA). In its waning days, is the Trump administration aiming to exit the GSEs from conservatorship? Capital Commentary explores this topic in this issue. Follow the links for deeper dives.

1. Step One: Raise GSE Capital Requirements

FHFA’s most prominent step was to issue a final rule establishing a new capital framework for the GSEs on Nov. 18. The final rule is largely consistent with a proposed rule that was issued for public comment in May.

- Why is the final rule important? It puts Fannie Mae and Freddie Mac on a path toward a sound capital footing, said FHFA Director Mark Calabria. “The final rule is another milestone necessary for responsibly ending the conservatorships.”

- The numbers: An aggregate of $283.4 billion in risk-based capital will be required for both GSEs, up from $262.7 billion in the earlier proposal. They will need to hold the greater of the risk-based minimum or 4% of their total assets ($265 billion as of June 30), which is known as the leverage ratio.

- Loan costs will rise: At current interest rates, the new capital levels could push up the price of a loan by 10%, or an average of $15,000 over the life of the typical loan, said Seamus Fearon, Executive Vice President of Credit Risk Transfer and Services, Arch Capital Group Ltd.

In its announcement, FHFA highlighted changes it made to its original proposal to increase capital relief for the GSEs through credit risk transfer (CRT). CRT experts in the housing and insurance fields were quick to take issue with that conclusion (See item #3).

2. Step Two: Persuade Sec. Mnuchin to Sign On

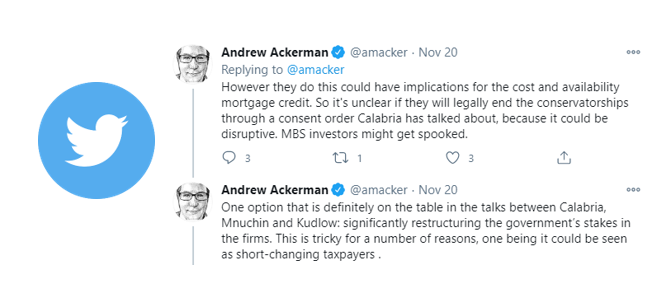

Joe Biden’s win in the 2020 presidential election appears to have expedited FHFA’s effort to privatize the GSEs. But FHFA needs the support of Treasury Secretary Steven Mnuchin to accomplish the task. The Treasury Department owns more than $200 billion in preferred shares of Fannie and Freddie.

- The pace quickened because most observers believe the Biden administration will not move forward with exiting the GSEs from conservatorship.

- Calabria and Mnuchin have met at least twice, reports Andrew Ackerman of The Wall Street Journal (subscription required). “The Treasury Secretary must agree to any move to alter the terms of either of the companies’ bailout agreement or the government’s stakes.”

- The process would be complicated, and the ramifications for borrowers and lenders could be considerable, tweeted Ackerman.

“Reducing the government’s stake in Fannie and Freddie would involve recapitalizing the GSEs, then opening them to private investors through an initial public offering,” reports the investment-news website 24/7 Wall St. “One significant issue with this path is that private investors who scooped up shares of Fannie and Freddie following the 2009 bailout want to be paid, not wiped out.”

Not so fast, say critics. Several experts, policymakers and trade groups quickly opined:

- “It would be extremely disruptive to the housing-finance system at a terrible time,” housing consultant Jim Parrott told MarketWatch.

- “In compensation for this investment, the taxpayer has been given warrants on 79.9% of the GSEs’ common stocks and approximately $222 billion in preferred shares, which carry an annual dividend,” wrote U.S. Sens. Mike Rounds, R-SD, and Mark Warner, D-VA, in letters to Mnuchin and Calabria. “We want to remind you of the importance of honoring the taxpayers’ ownership interest in the GSEs in future administrative actions.” (Inside Mortgage Finance, subscription required.)

- “While we believe that responsible, incremental steps as part of a holistic and well-understood housing finance reform plan should continue to proceed, [the Structured Finance Association] urges the Treasury Department to not make any sudden, major substantive changes to the Preferred Stock Purchase Agreements (PSPAs) that would place the GSEs on an irrevocable path out of Conservatorship” until significant questions can be addressed. (Full SFA letter to Mnuchin.)

- The National Association of Realtors® called on FHFA and the Trump administration to apply the brakes to any efforts to expedite an exit from conservatorship for the GSEs. “[NAR] urges the Treasury and FHFA to forestall advancing the pre-finalized enterprise capital rule and making any changes to the preferred stock purchase agreements that could endanger market stability by ending the conservatorship. The agencies must be prudent in exercising regulatory restraint in the best interests of the recovering economy until after the pandemic is under control,” wrote the trade group in a Nov. 30 letter to Mnuchin and Calabria.

A Washington Post editorial, “Why Rushing to Privatize Housing Finance Is a Bad Idea,” concludes, “If it ain’t broke, don’t fix it. Fannie and Freddie are broken in one sense – they collapsed – but quite sound in another: The government propped them up so comprehensively that mortgage markets now function normally.”

3. GSEs Likely to Retain Future Credit Risk

Since 2013, Fannie and Freddie have successfully transferred 70% of their credit risk to capital markets and reinsurers. CRT is less expensive than common equity, protects taxpayers and provides the GSEs with critical information about the perceived risk of the loans they are buying.

- But CRT may not survive the new GSE capital standards, which reduced CRT’s capital-relief value by about 50%.

That means Fannie and Freddie are likely to revert to the tried-and-failed model of buying and holding credit risk that led to their being placed into conservatorship.

FHFA’s choice to lower CRT’s value already led Fannie Mae to put a pause on its future CRT transactions.

- “CRT didn’t exist during the last housing crisis,” Joe Monaghan, CEO of Aon’s public sector partnership, said recently. Aon is a reinsurance broker. “It is a great innovation that is working” to both lower borrower costs and inform the GSEs of the risks they are taking on. “Why would we go backward?”

- Industry analyst Isaac Boltansky of Compass Point LLC wrote in a recent report, “We remain concerned regarding the economic viability of CRTs under the FHFA’s capital framework.”

- “The credit risk transfer program, supported overwhelmingly by the industry, elected officials from both parties and all but a few extreme GSE-skeptic policy specialists, would have, under the proposed capital rule, dramatically declined if not outright ended, wrote former Freddie Mac CEO Don Layton in a blog post for the Joint Center for Housing Studies at Harvard University. “The FHFA says the final rule is more generous in its allowance for CRT to offset credit risk, but the numbers indicate otherwise.”

4. Should the GSEs Remain in Conservatorship?

That is one of two recommendations recently offered by Layton in a recent report published for the Joint Center for Housing Studies.

Layton offered his suggestions to the incoming Biden administration on the question of “What to Do about Fannie Mae and Freddie Mac”:

- “The first possible path is to leave the companies in long-term conservatorship — which has worked, continues to work unexpectedly well — and then possibly revisit the question of conservatorship exit in a few years,” he wrote.

- A second possible path would be to transition the current GSEs through administrative steps to a utility model where their fees and earnings would be tightly regulated.

Layton argues that given the plethora of issues confronting the new administration, GSE reform isn’t worthy of much attention.

- “First, the mortgage system is working well and many industry players say it is performing very well. The average homeowner does not see anything that is particularly broken,” he wrote.

- “Second, for many years people in housing finance claimed that it would be ‘unsustainable’ for the two GSEs to stay in conservatorship for an extended time. Theoretically, that should be true. However, more than 12 years later, the hard reality is that conservatorship is, in fact, looking very sustainable.”

- “Third and last, by and large the ‘industry’ … ha[s] become generally happy with how the GSEs have been operating for the last roughly seven or eight years. In my view, most are nervous that any changes due to a particular reform plan might be problematic and harmful to their interests, and so are relatively content with the status quo.”

The bottom line, says Layton, is that the Biden administration should not especially prioritize housing finance reform in its first 12 to 24 months. “It has far more impactful domestic economic policies to focus on instead,” he concludes.

If record-low interest rates weren’t sufficiently satisfying, home loan borrowers now have another reason to smile: In late November, FHFA announced it is raising conforming loan limits (loans that can be purchased by Fannie and Freddie) by 7.42%. The new limit for most parts of the U.S. is $548,250, an increase of nearly $40,000 over the current cap. In high-cost metro areas, borrowers of loans up to $822,375 can have their loans acquired by the GSEs. Loans purchased by the GSEs are generally less expensive than so-called non-conforming loans.

Do you think Capital Commentary offers valuable information on housing policy and its potential impacts? If you do, share your comments with us. Your feedback will help ensure Capital Commentary covers the stories that have the most impact on your business.

About Arch MI’s Capital Commentary

Capital Commentary newsletter reports on the public policy issues shaping the housing industry’s future. Each issue presents insights from a team led by Kirk Willison.

About Arch MI’s PolicyCast

PolicyCast — a video podcast series hosted by Kirk Willison — enables mortgage professionals to keep on top of the issues shaping the future of housing and the new policy initiatives under consideration in Washington, D.C., the state capitals and the financial markets.

Stay Updated

Sign up to receive notifications of new Arch MI PolicyCast videos and Capital Commentary newsletters.