The “generational housing war” has become one of the loudest, least-informed debates in American life. Notably, most of the numbers fueling it don’t mean what people think they mean.

The big picture:

- Gen Z homeownership is at the lowest rate ever recorded.

- Gen Z is also arguably ahead of Millennials and Gen X at the same age, once the math is adjusted.

Both statements are true. Both get quoted constantly, usually by people trying to win an argument rather than settle one.

The stakes: As Congress, regulators and the housing industry debate who should benefit from housing policy next, it’s crucial to distinguish between generational statistics that are truly impactful and those that merely go viral. This distinction is vital for anyone involved in setting underwriting standards, credit policy or legislation.

1. Big Thing: Vanishing Starter Homes

Where do you start on the homeownership ladder without starter homes?

Why it matters: Decades of zoning favoring large-lot single-family homes have starved the market of starter homes — including townhomes, small, single-family residences and condos. That’s the entry rung of the ladder, and it’s rusted through.

- Even in areas where starter homes exist, they are unaffordable for more than six in 10 households, according to new research from Lending Tree.

By the numbers: The average starter home nationwide costs $200,000, reports Lending Tree. The median non-homeowner household earns $7,099 less than the $62,099 annual income needed to purchase one.

What happened? The math stopped working. Particularly for younger households.

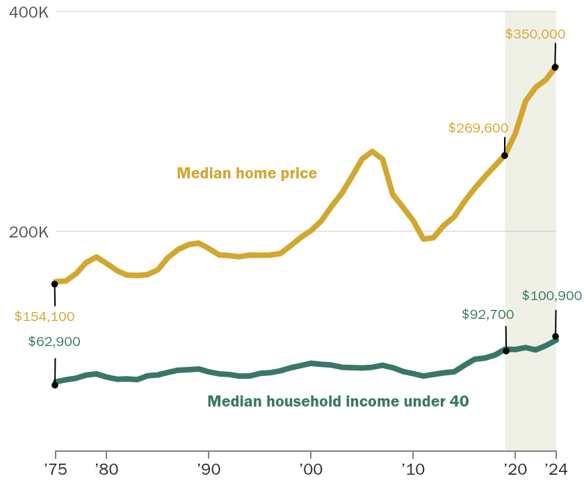

Fifty years ago, the median-priced U.S. home was 2.45 times the median income of households headed by someone under 40. Today, that ratio has ballooned to 3.5 times.

National median home prices and incomes for households under 40 in 2024 dollars. Source: Pew Research Center

The golden handcuffs of low-interest-rate mortgages only worsen the housing shortage. Baby Boomers and Gen X generations just aren’t moving house as they did in years past, largely because they don’t want to trade a 3% mortgage for a 6% one.

Add to it the burdens of student debt, high rent costs and a questionable job market for new college graduates and, well, the homeownership jam facing Gen Z isn’t going away anytime soon.

- That’s the conclusion of two Morgan Stanley experts, who described the challenges in a recent podcast.

What they’re saying:

“We do think that the housing market is resetting at a structurally higher barrier to entry.” — Sarah Wolfe, Senior Economist, Morgan Stanley

2. The Stat War, Decoded

There are two competing “Gen Z homeownership rate” statistics circulating — and they are not measuring the same thing.

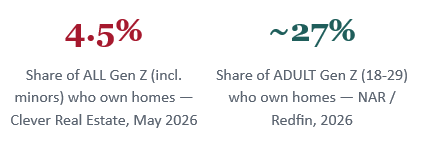

The 4.5% figure — the one dominating the news, from Clever Real Estate — divides homeowners by the entire generation that is generally defined as ages 14 to 29. Of course, many in that age group are years from considering homeownership. (Clever, indeed, if you want to make headlines!)

- But if you adjust for age, Gen Z’s homeownership trajectory looks comparable to, or slightly ahead of, Millennials and Gen X at the same age, per the National Association of Realtors® (NAR) and the Berkeley Institute for Young Americans.

Why it matters: The real story isn’t that Gen Z can’t buy … it’s that fewer Gen Zers can buy as early as their parents did, and those who do are using different tools to get there. More on that in Item 5 below.

3. And the Blame Goes to …

Depends who’s asking.

The timing argument: Boomers entered the market in the 1970s–1980s, when home prices were low and new construction was booming, even with double-digit mortgage rates. As a result, 73.1% of Baby Boomers now own their homes, according to Clever Real Estate.

- Gen Z may just be unlucky in when they were born.

The policy argument: Boomers vote and they often vote to protect home values — which means opposing the very zoning and density reforms that would fix the missing-middle problem. They also aren’t leaving leadership positions in numbers that would accelerate policy change.

“The Times, They Are a-Changing,” wrote Silent Generation member Bob Dylan. He could have been describing the differences between Boomers and Gen Z.

What they’re saying: Let Kyla Scanlon, Gen Z’s most followed economics commentator (600k+ followers), explain:

“The Boomer generation … had a somewhat clearish wealth-building formula: Career progression + home appreciation + retirement savings, supported by mostly predictable returns on education. They are the wealthiest generation to have ever lived.”

Gen Z has taken a different path to adulthood, she argues.

“When a single viral TikTok can outperform a year’s salary, and traditional credentials lose value faster than you can earn them, young people aren’t just changing careers —they’re developing fundamentally different relationships with economic reality … the ‘safe path’ (corporate job, 401k) might be the riskiest bet.” The result? “They’re very mad,” Scanlon told Bloomberg TV. “They’re extremely anxious, and they’re extremely distrustful.”

Engage with Capital Commentary

Share your thoughts: We invite you to click here and share your insights on this issue.

Explore Arch MI Insights: Want to dive deeper? Click here to access past issues and listen to previous episodes of the Arch MI PolicyCast podcast.

4. It’s the Same Down Under, Too

Australians face similar homeownership barriers.

- Younger Australians are locked into historically high rents and home prices. The median home price in Australia is nearly AUS $1.3 million. In the Sydney metro area, where one in five Aussies live, the median price exceeds AUS $1.7 million.

Australia’s Senate earlier this year created a Select Committee on Intergenerational Housing Inequity to address the crisis.

The committee is tasked with evaluating the nature of intergenerational housing inequity in Australia across housing types and populations. Additionally, the Senators are asking which factors are affecting housing reform and which services, laws and policies would be most effective in reducing the inequity in Australia.

What they’re saying: “The third hearing of the … Senate inquiry into intergenerational housing inequity, has painted a picture of younger generations being ripped off, locked out of the housing market, forced into insecure housing and delaying major life decisions,” reads a press release from the Greens Party.

Among the findings to date:

- 81% of Gen Z and Millennials say the cost of housing has affected the timing of major life decisions.

- 35 years ago, most low-income younger households owned their own home. Today, only about one in five do.

- There’s a growing reliance on the “bank of mum and dad.” More than 57% of parents have helped their children buy a home over the past 10 years.

What’s next: The Select Committee is expected to issue its final report and recommendations by the end of September

5. The Other Side of the Ledger

Gen Z is buying — just not the way their parents did.

A larger share of Gen Zers are attending college, many continuing on for graduate and professional degrees. They are marrying and having children later, too. It should be no surprise that homeownership is coming later.

But Mark Fleming, First American’s Chief Economist, is optimistic about the generation’s chances for homeownership. He cites two charts as reason for hope.

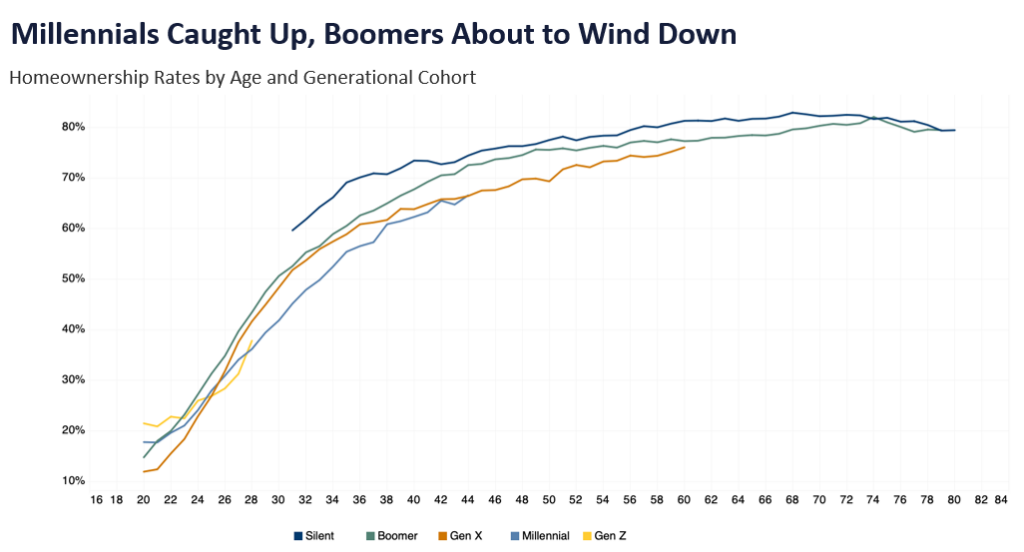

Fleming notes that Gen Z is ahead of Millennials in the share of homeowners at 28 years old. Millennials, meanwhile, caught up to Gen X’s homeownership rate by age 44. That is steady progress by both generations.

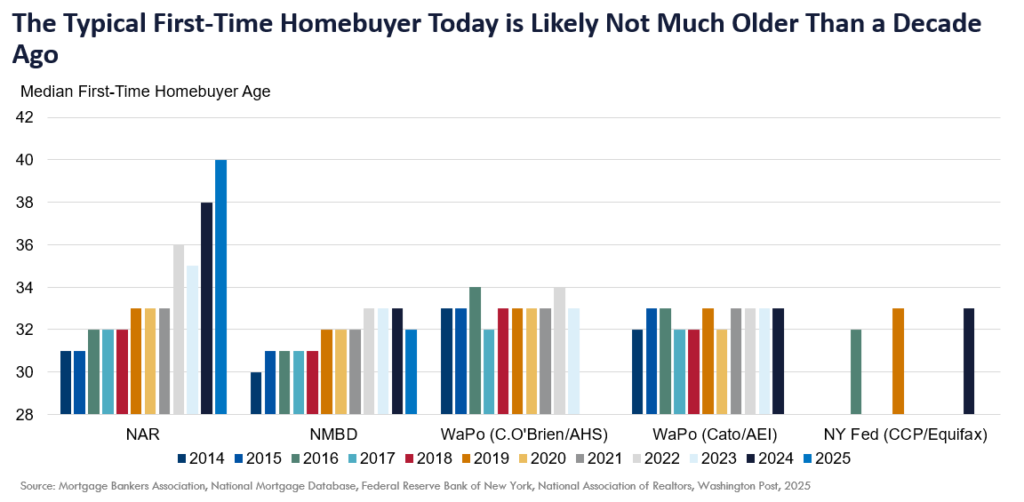

Fleming also discounts news stories citing an NAR finding last year that the average age of first-time homebuyers hit 40 years old. NAR’s statistics are an outlier, he argues.

- The numbers from other sources have stayed flat over the past decade at 32 to 34 years old.

How else are Gen Z homebuyers different than previous generations?

- 35% of Gen Z homebuyers are single women, the highest share of any generation on record (vs. married-couple having a 50% share across all buyers).

- 17% are unmarried couples — also a generational high. Most aren’t waiting for marriage or kids to buy.

They’re using tools their parents didn’t.

- 78% of Gen Z buyers used down-payment assistance programs — more than any other generation — and only 16% got a parental gift or loan, well below the historical 25% average.

6. Boosting Gen Z Homeownership

U.S. policymakers took an important step in enacting the 21st Century Road to Housing bill, the most significant housing legislation in decades. But more needs to be done to achieve homeownership equity in the U.S.

Here are my recommendations:

- Legalize the missing middle. A growing bloc of younger, cross-partisan legislators is pushing to unwind zoning that bans duplexes, townhomes and accessory dwelling units in commercial and residential zones alike — matching supply to where demand is.

- Lower costs for smaller mortgage loans. More small-dollar mortgage products and smaller, less expensive housing stock need financing partners willing to serve that segment — not just zoning reform.

- Widen the credit aperture. Incorporating rental payment history and utility payments into underwriting, with appropriately measured risk pricing, could pull historically excluded, credit-invisible borrowers meaningfully closer to mortgage-ready. Both VantageScore® 4.0 and FICO® 10T use such data in their credit scores.

- Use the whole lender toolbox. Down-payment assistance and first-time buyer programs remain under-used relative to eligibility. Too many borrowers mistakenly think they need a 20% down payment to purchase a home, even though loans insured with mortgage insurance (MI) or FHA can make homeownership possible with 3% or 5% down.

The bottom line: Gen Z’s path to homeownership won’t look like their parents’ journey.

Policy and lending that meet them on those terms, rather than insisting on the old ways, are what will move the needle.

There will be more solo buyers, more assistance programs and they will need more patience.

About Arch MI’s Capital Commentary

Capital Commentary newsletter reports on the public policy issues shaping the housing industry’s future. Each issue presents insights from a team led by Kirk Willison.

About Arch MI’s PolicyCast

PolicyCast — a video podcast series hosted by Kirk Willison — enables mortgage professionals to keep on top of the issues shaping the future of housing and the new policy initiatives under consideration in Washington, D.C., the state capitals and the financial markets.

Stay Updated

Sign up to receive notifications of new Arch MI PolicyCast videos and Capital Commentary newsletters.

About the Author