Welcome to the first 2026 Daylight Saving Time edition of Capital Commentary!

Situational awareness: The role of institutional investors in housing affordability is under scrutiny as President Trump highlights a proposed ban in his speeches and the U.S. Senate advances a housing bill containing such a restriction.

📅 Fate unclear: The comprehensive housing bill is progressing in Congress, but the portion restricting investors remains uncertain. This issue of Capital Commentary dives into the pros and cons of an institutional investor limit.

1. Big Thing: The Ban in Brief

“Corporations shouldn’t own homes, people should,” Trump said in his Feb. 24 State of the Union Address, urging a prohibition on large investor purchases of single-family homes.

Trump previously signed an Executive Order in January directing key agencies to issue guidance preventing relevant Federal programs from approving, insuring, guaranteeing, securitizing or facilitating sales of single-family homes to institutional investors.

- The Senate followed suit, writing companion legislation and attaching it to the 21st Century ROAD to Home Act, which passed on March 12 by an 89-10 vote. Yet the ban’s ultimate fate is still unclear as House Republicans have concerns about it.

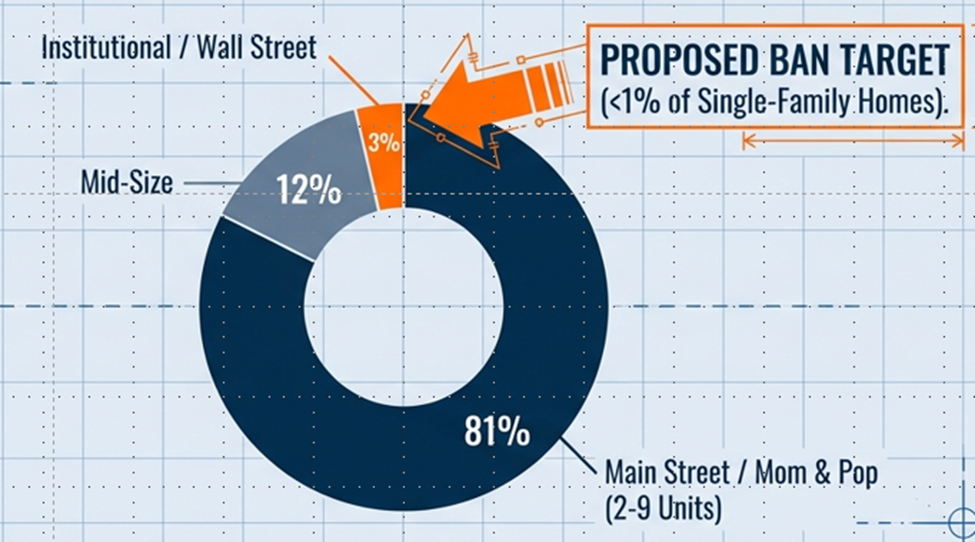

The big picture: The restriction on future purchases of single-family homes applies to entities owning more than 350 homes.

Yes, but: There are exceptions written into the bill, including:

- Investors who report positive rental payments and give renters the right of first refusal when selling the home.

- New construction of build-to-rent (BTR) housing. But the Senate bill would also require investors to sell those homes within seven years.

2. Pro-Ban: Hedge Funds Ate Your Neighborhood

President Trump’s populist push against institutional investors buying homes taps into a national sentiment, with Treasury Secretary Scott Bessent revealing it ranks just behind border and grocery issues in voter concerns.

Why it matters: Advocates argue these large investors restrict consumer choice and inflate home prices.

- Major players like Blackstone and Invitation Homes are accused of frequent evictions and contributing to a housing affordability crisis.

Broad support: The legislation is backed by key figures like Sens. Bernie Sanders, I-Vermont, and Elizabeth Warren, D-Massachusetts, as well as tenant rights associations and consumer advocates.

Senate Democrats’ alternative: Their “American Homeownership Act” proposes cutting tax incentives for large investors, shifting benefits toward families.

What they’re saying:

- Sen. Jeff Merkley, D-Oregon, contends, “Hedge funds are inflating housing costs, hindering homeownership dreams.”

- Sen. Tammy Duckworth, D-Illinois, adds, “Tax breaks should aid families, not profit-driven corporations.”

Regional impact: In metro Atlanta, investors own 30% of single-family rentals, a stark contrast to national norms. In Henry County, where the population is majority Black, and Paulding County, which is majority white, large investors control 64% and 78% of rentals, respectively.

By the numbers:

- Some institutional investors owning homes in Fulton County, Georgia were 18% more likely to file eviction notices than smaller landlords, according to a Federal Reserve Bank of Atlanta study.

- A House Financial Services Committee report found that institutional investors specifically target neighborhoods with larger Black populations and a concentration of single‑mother households about 30% higher than the national average.

My thought bubble: In Washington, perception is reality. President Trump and progressive Democrats see a prohibition on institutional investor home purchases as a popular solution to a growing affordability problem.

- Whether the effort succeeds won’t be known for years. That matters less than the fact voters will go to the polls in eight months to determine control of Congress.

- Voters want housing affordability addressed, and the sooner the better.

3. Anti-Ban: “The Rental Relief Bill That Isn’t”

“We might as well call this the ‘rental inflation’ bill,” writes housing firm John Burns Research & Consulting in a recent blog.

- While the bill “aims to make housing more affordable, [it] includes provisions that will make housing more expensive,” wrote the blog’s authors.

Why it matters: Opponents of the proposed restriction cite statistics showing institutional investors owning 350+ rental homes own 0.7% of all single-family homes in the country, and have been reducing their purchases since 2022.

Proponents ignore the benefits institutional investors have brought to the housing market, argues Anne Canfield of The Majority Group, a Washington firm that represents residential real estate investors.

What they’re saying:

“They have added critical rental supply, rehabilitated distressed properties, modernized aging housing stock and supported build-to-rent communities. Acting as a reliable ‘shock absorber,’ they inject liquidity during downturns (as seen after the Great Recession) and help absorb demand shocks in high-growth areas.” — Anne Canfield

- Other voices, too, are raising concerns about the prohibition, particularly the requirement that investors would have to sell homes after seven years.

- Sen. Brian Schatz, D-Hawaii, called the mandate to sell rental housing “positively Soviet,” adding, “We have decided, for no particular reason other than what I think is a drafting error, to demonize people who want to build rental housing.”

Most renters aren’t ready to be homeowners, cautions Tobias Peter of the American Enterprise Institute.

“If Washington pushes these investors to divest, not only will investor-owned homes come on the market, political pressure will likely follow to loosen credit standards. Lawmakers want these homes transferred from investors to owner-occupants. The problem is that many of the tenants renting these homes are not mortgage ready under normal underwriting standards.”

Peter fears Washington may first force homes onto the market and then force financing to match the politics.

“It may help facilitate transactions in the short run. But it raises the risk of future delinquencies, distressed sales and broader market instability.”

Engage with Capital Commentary

Share your thoughts: We invite you to click here and share your insights on this issue.

Explore Arch MI Insights: Want to dive deeper? Click here to access past issues and listen to previous episodes of the Arch MI PolicyCast podcast.

The bottom line: If the primary cause of unaffordable homes is the lack of housing supply, the investor limit will only exacerbate the problem, concludes the John Burns firm.

“We track approximately 500,000 units in our BTR database, including 160,000 coming soon. If a disposal requirement remains in the final bill for any product type, we would expect fewer to be built. We have already seen a significant pullback in BTR starts, and the seven-year disposal requirement would only accelerate this reduction in supply.”

4. Will the House Decide Housing’s Future?

The fate of the most comprehensive housing bill in decades rests with the U.S. House of Representatives.

Why it matters: Bipartisan support for streamlining federal regulations and modernizing manufactured housing rules could pave the way for significant progress in housing policy.

The challenge: Senate language aimed at restricting large investor-owned rental homes poses a significant threat, risking delays or even the collapse of the legislation.

Opposition: A growing coalition, including the Mortgage Bankers Association and other key housing groups, opposes the requirement that investors dispose of rental properties after seven years. They are advocating for this section to be removed from the bill.

What’s next: According to a Washington insider, the House is unlikely to accept the Senate bill as is, with two possible paths forward:

- The House could amend the bill and send it back to the Senate.

- Alternatively, a conference between the House and Senate may occur to reconcile differences in the housing bills passed by each chamber.

5. PolicyCast LIVE! March 18: How to Save a House from Destruction

Skyrocketing homeowners insurance premiums are not only making qualifying for a home purchase more difficult, they are increasing the risk of delinquency and default for existing owners, too.

Can a crisis be averted? John Rogers knows.

Watch the PolicyCast LIVE Replay featuring Rogers, who is Cotality’s (formerly CoreLogic) AI and data guru. Get more details on Arch MI’s LinkedIn page.

- Rogers is an expert in analyzing billions of units of data to tell homeowners what they need to do to reduce their risk and, just as important, lower their premiums.

About Arch MI’s Capital Commentary

Capital Commentary newsletter reports on the public policy issues shaping the housing industry’s future. Each issue presents insights from a team led by Kirk Willison.

About Arch MI’s PolicyCast

PolicyCast — a video podcast series hosted by Kirk Willison — enables mortgage professionals to keep on top of the issues shaping the future of housing and the new policy initiatives under consideration in Washington, D.C., the state capitals and the financial markets.

Stay Updated

Sign up to receive notifications of new Arch MI PolicyCast videos and Capital Commentary newsletters.