Was it an April Fools’ Day headline or real news when the Los Angeles Times’ lead story proclaimed, “People Who Leave California Find Much Lower Costs”?

Why it matters: Every so often, a new housing study lands with impeccable methodology, elegant charts … and a conclusion your neighbor could have delivered over coffee.

- The latest entry, the California Policy Lab finding that people who leave California locate cheaper housing, inspired us to look at similarly “shocking” conclusions.

Not to mock them. (Well, maybe a little.)

Since this is April and Congress stopped working in Washington for two weeks (that’s not a joke, either), let’s use this edition of Capital Commentary to review a few of the top housing studies that confirmed … what everyone already knew!

1. Big Thing: Would You Believe … ?

They commissioned a study … and it turns out expensive housing is expensive.

Why it matters: A new California Policy Lab study confirms that when people leave California for less expensive states, their housing costs go down — and their chances of owning a home go up.

The bottom line: That’s not a punchline. That’s the headline.

Go deeper: The California Policy Lab research covered people who left or arrived in California from 2016 to 2025 — millions in total.

The top choices to make a new start were states such as Nevada and Arizona, but also included Texas and Florida. And those who left — also not surprising — were less affluent than the ones who stayed behind.

By the numbers: Leavers had twice as much student debt and 16% higher rates of credit card use.

“California, Here We Depart”:

- Moving to another state reduced housing costs by about $672 a month.

- 48% are more likely to own a home after seven years.

- Even with slightly lower incomes, they come out ahead on affordability.

What they’re saying: The California housing situation is a “really sad story,” said Dowell Myers, a professor of policy, planning and demography at the University of Southern California. .

As to young professionals, Myers laments that, “we can’t hold them, that’s the lesson. They come for opportunities, but housing is really key.”

2. More ‘Shocking’ Conclusions

Consider a few recent examples:

- If you can’t afford to live near work, your commute gets longer.

Go deeper: This study from the University of California’s Institute of Transportation Studies examines residents in coastal and inland areas of Southern California. It found that suburbs now house more people living below poverty than urban areas.

– In practice, affordability constraints are pushing lower-income households farther from job centers, resulting in longer and often more complex commutes.

What’s less intuitive:

– Commute distance doubles but time doesn’t.

– Nearly 30% of inland workers commute back to coastal job centers. (As a native Californian, I can attest: brutal.)

Why it matters: Housing pressures don’t just reshape commutes — they reshape access to ownership.

- Expensive homes reduce homeownership.

Researchers at UC Berkeley’s Terner Center for Housing Innovation found that the rise in housing prices in California has had a major impact on access to homeownership, above and beyond other drivers of people’s choice to buy a home.

The reality behind the data: The researchers found that if home prices since 2000 had risen only as fast as the rest of the nation, an additional 735,000 Californians would be homeowners.

What’s less intuitive:

– Median Californian net worth is about 70% higher than the national median, yet they are less able to afford homes at every age.

– Share of seniors owning homes free and clear is declining. In California, more retirees are still paying off mortgages, resulting in greater long-term financial vulnerability.

And for many households, the pressures don’t stop at affordability — they extend into housing stability itself.

- Evictions destabilize households.

It is well understood that evictions can increase homelessness, reduce earnings and limit access to credit. What this research from Yale adds is a clearer understanding of how — and when — those effects take hold.

The study provides rigorous evidence confirming — and refining — that understanding.

A striking datapoint: According to the study, among the 38 most advanced and economically developed nations, the U.S. has the highest number of evictions per renting household.

What’s less intuitive:

Eviction isn’t the spark — it’s the smoke from a fire already burning. Hospital visits and financial distress are rising long before eviction.

Eviction does not move people into worse neighborhoods. Most people end up in similar-poverty neighborhoods as before. The more concerning issue is not relocation, it’s the instability that follows.

The bottom line: The headlines may feel familiar. The implications are anything but.

3. Who Killed Affordable Housing?

In all seriousness, it’s easy to look at these various reports and say: “We needed a study for this?” But that misses the point.

In policy, the goal isn’t to prove something is intuitive. It’s to prove:

- How large the effect is.

- Whom it impacts most.

- Whether it’s causal.

That’s the difference between a talking point and something you can defend in front of regulators, lawmakers or investors.

What ties these findings together isn’t the obviousness — it’s the direction. People are:

- Moving farther from jobs.

- Delaying or forgoing homeownership.

- Leaving high-cost states.

- Or, in some cases, falling out of housing altogether.

Why it matters: They are all responses to the same underlying constraint: housing costs outpacing incomes.

By the numbers: The median household income in the U.S. is roughly $80,000. The income needed to purchase the median-cost home is $123,000.

- That “affordability chasm” is the largest in history.

The bottom line: Yes, a lot of housing research confirms what people suspect. But here’s the uncomfortable reality embedded in this latest study:

For many households, the most reliable affordability strategy is no longer to adapt … it’s to leave.

And when that becomes the equilibrium, it’s no longer just an academic finding.

- It’s a signal that policymakers at all levels of government, in Washington, state capitals and city halls, need to work harder on finding solutions to build more homes and make housing affordable again.

Engage with Capital Commentary

Share your thoughts: We invite you to click here and share your insights on this issue.

Explore Arch MI Insights: Want to dive deeper? Click here to access past issues and listen to previous episodes of the Arch MI PolicyCast podcast.

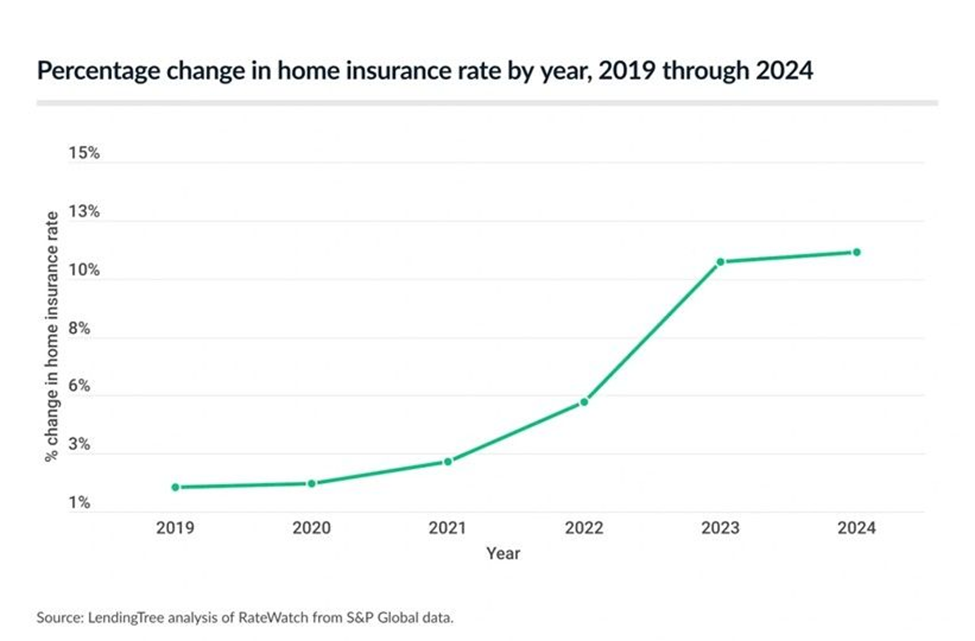

4. Home Insurance Premiums are Becoming a Disaster

Skyrocketing homeowners insurance premiums are not only pushing debt-to-income ratios higher for prospective homebuyers but also putting many existing homeowners at financial risk.

John Rogers, Cotality’s Chief Data and Analytics Officer, provided a deep dive into why homeowners are paying more for insurance and how they — and homebuilders — can mitigate natural disaster risks on the latest Arch MI PolicyCast.

About Arch MI’s Capital Commentary

Capital Commentary newsletter reports on the public policy issues shaping the housing industry’s future. Each issue presents insights from a team led by Kirk Willison.

About Arch MI’s PolicyCast

PolicyCast — a video podcast series hosted by Kirk Willison — enables mortgage professionals to keep on top of the issues shaping the future of housing and the new policy initiatives under consideration in Washington, D.C., the state capitals and the financial markets.

Stay Updated

Sign up to receive notifications of new Arch MI PolicyCast videos and Capital Commentary newsletters.